Free Trade or Economic War?

Anyone going to school in the U.S. after WW II has learned the breakdown in world trade was a primary, though not only, cause of …

Anyone going to school in the U.S. after WW II has learned the breakdown in world trade was a primary, though not only, cause of …

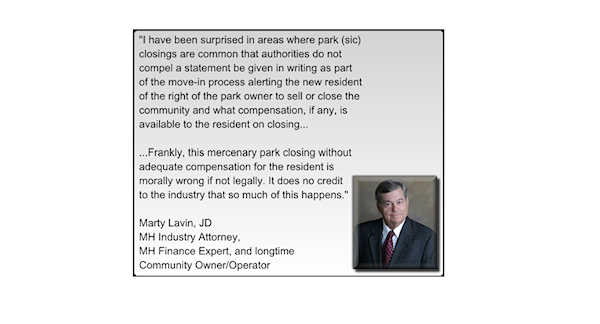

As with many things in life, the matter of park closings is highly complicated with few easy answers. Probably the best answer is to allow …

A New Study I like to say to myself “If you live long enough, you’ll see it all.” I have now lived long enough to …

DÉJÀ VU AGAIN? A New Manufactured Housing Institute (MHI) Initiative Read More »

With apologies to MH Industry legend Randy Rowe and his 5 Point Plan for Industry Recovery – which is insightful and important reading – let me …

Dare’s 3 Point Plan for Manufactured Housing Industry Recovery Read More »

Phew! After reading the Seattle Times news article on Clayton Homes and Vanderbilt Mortgage, I am reminded of a scene in the movie, “No Country for …

Marty Lavin’s Views on Seattle Times-BuzzFeed Clayton Homes VMF-21st Controversy Read More »

I think around 2005 or so I was at the Wisconsin Association giving my latest Doom and Gloom prognosis for the future of our industry. …

Tony, I've been delighted with the self-financing articles and feedback you have gotten on the subject. I've never doubted self-finance can be done properly, but …

Captive Finance Redux: Are you dealing with the Gestapo/NSA or Colonel Klink? Read More »

Marty, before we get into the meaty topics that will follow, let's establish your credentials for readers who may not know you and your background. …

New York Times Columnist, Tom Friedman, wrote a thoughtful column about the hard truths leaders around the world seem unwilling and unable to tell their …

There is a lot to say about what has gone wrong with our country and our Industry. We will begin ‘at the top,’ with our …