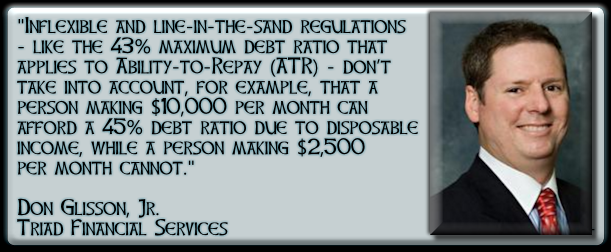

Don Glisson Jr. – CEO of Triad Financial Services – on Dr. Ben Carson for HUD Secretary

We at Triad Financial Services are hopeful that President-elect Trump and soon-to-be HUD Secretary, Dr. Ben Carson, are committed to sensible regulation for manufactured housing …

Don Glisson Jr. – CEO of Triad Financial Services – on Dr. Ben Carson for HUD Secretary Read More »