Free Trade or Economic War?

Anyone going to school in the U.S. after WW II has learned the breakdown in world trade was a primary, though not only, cause of …

Anyone going to school in the U.S. after WW II has learned the breakdown in world trade was a primary, though not only, cause of …

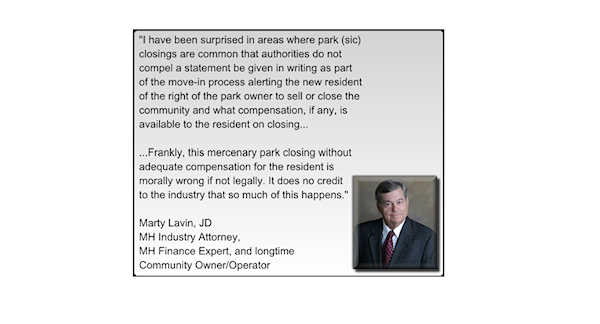

As with many things in life, the matter of park closings is highly complicated with few easy answers. Probably the best answer is to allow …

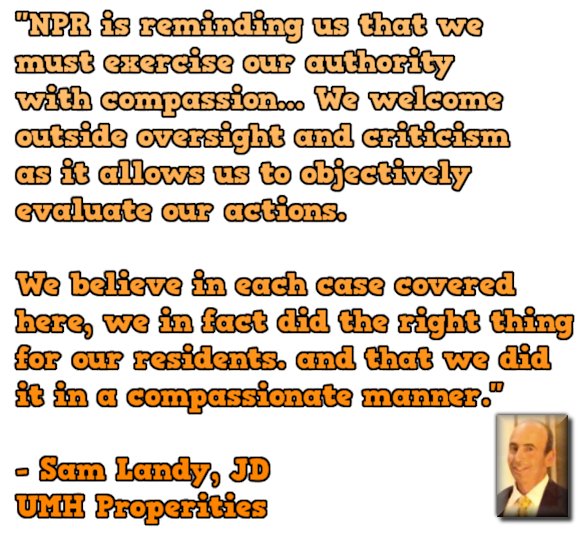

NPR and UMH both care deeply about people. UMH has operated manufactured home communities since 1969. We believe enforcement of our rules and regulations is …

UMH Properties’ Sam Landy Reacts to Call to Defund National Public Radio (NPR) Read More »

National Public Radio (NPR) did a two-part report released this week on manufactured home communities, part one of their controversial story – “Mobile Home Park Owners …

I received your email on the article that highlighted the amenities package on which the counsel person in Austin was planning to introduce legislation. It …

About Government Forcing Manufactured Home Communities to Pay for Amenities Read More »

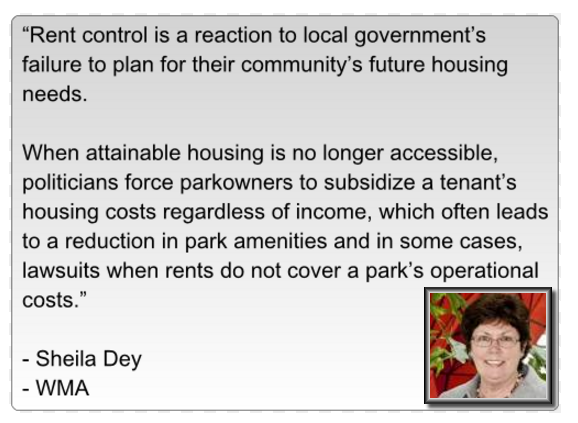

Costly government regulations have stifled the development of attainable housing October 14, 2016 (Sacramento, CA) – In an effort to educate public policymakers on how mobilehome …

California Housing Crisis: Manufactured Homes Could Be Part of the Solution Read More »

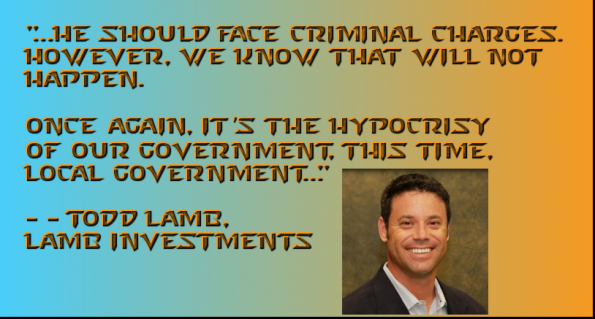

Tony, I agree with the Daily Business News article and the comments from other manufactured home industry professionals regarding Councilman David McCartney in Baytown. He …

As I read the digital 2014 Tunica Show brochure and business building and profit protecting seminar line up, it became crystal clear why Retailers and …

Why Retailers and Community Operators should go to Tunica! Read More »

by Richard “Dick” Jennison As President and CEO of the Manufactured Housing Institute (MHI), I participated in a manufactured home communities focused event held this …

Communities Themes Point to Rebound and Revitalization Read More »

A question brought up by an individual at a real estate investment group meeting in Tacoma, WA did not get answered at that time so thought …

What is the the future of independent Manufactured Home Communities? Read More »