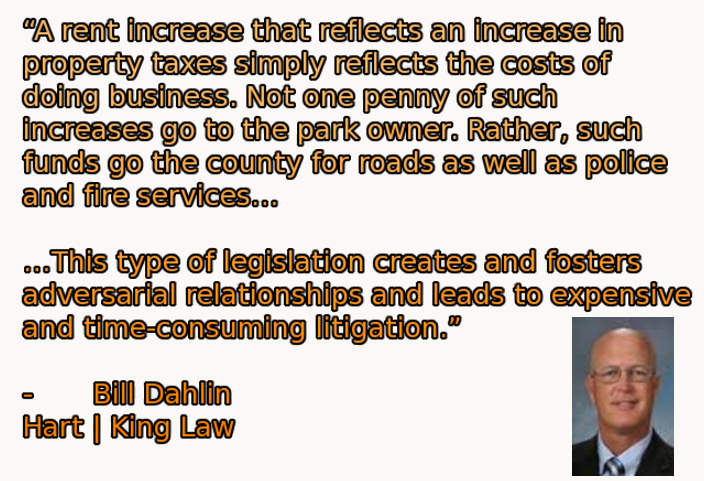

Measure V is Bad Public Policy, should be Rejected

Park owners in Humboldt County have been addressing the issue of alleged “excessive” rent for well over a year. Most Park owners offer long-term leases …

Measure V is Bad Public Policy, should be Rejected Read More »